Your Financial Review of October 2025

Turning Winds, Steady Compass

The third quarter of 2025 unfolded in a relatively stable climate yet marked by significant monetary adjustments. Central banks adopted a more accommodative stance: the Federal Reserve initiated its first rate cut since December 2024, followed by the Bank of Canada in September. These decisions were driven by risk management concerns in a context where signs of economic slowdown are beginning to multiply.

In Canada, inflation stabilized around 2%, in line with the target for several months. However, this lull was accompanied by turbulence in the labor market, with the unemployment rate rising to 7.1% in August, the same level as in August 2021. This contrasts with the eurozone, where both inflation and unemployment are at historically low levels, highlighting the fragility of Canada’s economic momentum.

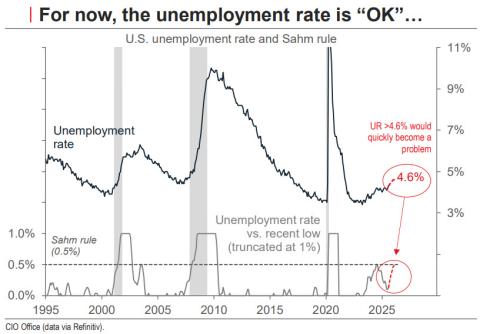

In the United States, the unemployment rate reached 4.3%, its highest level since October 2021. Although this level remains tolerable according to Fed projections, an increase beyond 4.6% could trigger the Sahm rule, signaling an increased risk of recession. Moreover, U.S. inflation remains stubborn at 2.9%, with service inflation stagnating and a rebound in goods and food prices, likely exacerbated by tariff policies.

Ultimately, while episodes of volatility may occur in the fourth quarter, the outlook remains constructive. The upward momentum in markets is expected to continue, supported by ongoing economic expansion in an environment of more conciliatory monetary and fiscal policies.

Market review as of September 30, 2025

Fixed Income

The Canadian fixed income universe ended the quarter in positive territory, supported by the shift in tone from the Bank of Canada and the Federal Reserve, both of which adopted a more cautious stance in September.

As of September 30, 2025, the FTSE Canada Universe Bond Index posted a quarterly return of +1.5% and +3% year-to-date. Canadian corporate bonds performed slightly better, with +1.8% in Q3 and +4.1% year-to-date.

Equities

Global equity markets continued their ascent in September, with strong leadership from Canada and emerging markets. The S&P/TSX1 delivered an exceptional performance of +12.5% in Q3, driven by the materials (+37.8%), energy (+12.6%), and financials (+10.6%) sectors.

Since the start of the year, international equities (MSCI EAFE2,3) lead with +25.7%, followed by Canadian equities (S&P/TSX) at +23.9% and U.S. equities (S&P 5002) at +14.8%.

Oil & Gold

Oil prices ($US/barrel) declined during the quarter, with WTI4 ending Q3 down -4.7%, for a year-to-date performance of -12.8%.

Conversely, gold prices2 continued their spectacular rise, gaining +16.7% in Q3 and +46.0% year-to-date. This dynamic strongly contributed to the performance of the materials sector in Canada.

Currencies

The U.S. dollar rebounded in Q3, after a sharp depreciation in the first half of the year. The Canadian dollar fell 1.9% against the greenback over the quarter, reducing its annual gain to +3.4%.

According to Goldman Sachs5, while the U.S. dollar is not close to be replaced in its international role, its overvaluation is expected to ease as U.S. economic performance becomes less exceptional. Stronger growth in Europe and China, combined with rising concerns over governance and currency risks, could increase downward pressure on the greenback in the coming months.

1. The S&P/TSX Index is the primary Canadian stock index measuring the performance of the Toronto Stock Exchange.

2. S&P500, MSCI EAFE and gold returns are expressed in US currency.

3. The MSCI EAFE Index is an equity index designed to measure the performance of equity markets in developed economies other than the United States and Canada.

4. West Texas Intermediate (WTI) Crude oil is the North American standard for setting oil prices. The returns are expressed in US currency.

5. Global Markets Analyst: Dollar dominance and Dollar Depreciation — moving on different tracks (Trivedi/Jenkins): https://publishing.gs.com/content/research/en/reports/2025/09/23/6609889f-e50e-4f3c-8222-5337fee64dfb.html

Investment Outlook

While the global economic environment remains complex, the coming quarters could be marked by improved financial conditions and increased support for fiscal and monetary policies. This context should support continued economic expansion, although some risks persist. A more pronounced deterioration in the labor market, particularly in the U.S., cannot be ruled out, nor can an acceleration in inflation that would challenge market expectations regarding Fed rate cuts.

After a relatively calm summer, markets may experience renewed volatility as they continue to digest ever-changing economic and geopolitical dynamics.

The Canadian market remains favored due to its more cyclical sector composition and valuations considered more attractive than those of the U.S. market.

Finally, although central banks have begun an easing cycle, bonds may continue to move without clear direction, hampered by a lack of visibility on the inflation trajectory and longer-term fiscal deficits.

In this context, our investment strategy remains cautious but moderately risk-positive. We continue to prioritize diversification and discipline, avoiding excessive bets in an environment still marked by political and economic uncertainty.

Thank you for your trust, and we remain fully available to discuss these perspectives and support you in optimizing your portfolio based on your objectives and market developments.

Sincerely,

Cathy, Guillaume, Marc-Antoine and Inuk

514-871-3474