Your Financial Review of April 2025

A Busy Start to the Year

In the span of just a few weeks, tariffs of 25% on imports from Canada and Mexico were announced by the Trump administration, then postponed, announced again, before being delayed for all goods compliant with the Canada-United States-Mexico Agreement. Then came April 2, 2025, the so-called "Liberation Day" of the Trump administration. On this date, the US administration announced the implementation of what it calls reciprocal tariffs, which varied from country to country – ranging from a minimum of 10% to a maximum of 49%. The methodology used by Washington to calculate these so-called reciprocal tariff equivalents raised several questions. Nevertheless, a genuine shock wave was observed in the markets. Indeed, the S&P 500 (the leading American index) fell by just over 12% between April 2 and April 8, bringing the index into correction territory – defined as a decline of at least 10% from a recent peak. In itself, this is nothing extraordinary. Since 1995, the S&P 500 has recorded an average correction of 16% per calendar year.

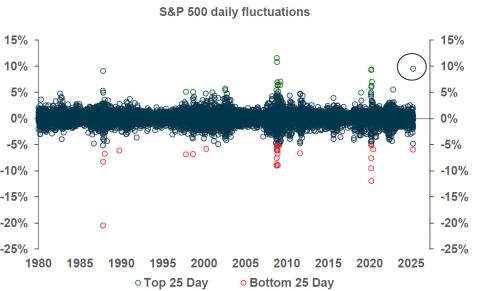

As has been the case several times since the beginning of the American tariff saga, on April 9, President Trump announced a 90-day pause on the "reciprocal tariffs" he had announced 7 days earlier, with the exception of those targeting China. This reversal propelled the S&P 500 upward, with the index closing the session at a level equivalent to a daily change of 9.52% (including 5.9% in just 15 minutes!). This volatility demonstrates the importance of not trying to "time" the market and reminds us that the best and worst days are often close together.

For its part, the Bank of Canada (BoC) currently finds itself facing a dilemma. Economic data was strong in the fourth quarter of 2024, and the first quarter of this year is temporarily boosted by strong exports, as American companies wanted to stock up on Canadian products before the potential implementation of tariffs.

Beyond concerns about tariffs and inflation, the BoC favoured a sustained tempo of its easing policy last year, outpacing central banks in major advanced economies. The BoC has nevertheless further lowered its overnight rate twice since the beginning of the year. The key rate currently stands at 2.75%. Now, various initiatives to mitigate the effects of tariffs, including a new push for interprovincial trade, deserve attention. Assuming that tariffs remain suspended, and that economic momentum is not further blunted elsewhere, our economics department envisions a key rate at 2.25% in 2025 and into the first half of 2026. This quasi-stimulative level would be appropriate for some time given the unused economic resources that remain to be absorbed.

Market review as of April 11, 2025

Fixed Income

The Canadian fixed income universe experienced a rather stable start to the year, with bond yields being held back by higher-than-expected inflation data and a Bank of Canada that has shown some reluctance to continue its rate-cutting cycle, at least in the short term.

As of April 11, 2025, the FTSE Canadian Universe Bond Index shows a performance of -0.17% since the beginning of the year, which is the same performance as the FTSE Canadian Corporate Universe Bond Index.

Equities

Notable changes in trends can be observed beneath the surface of equity indices. Geographical leadership has notably migrated from North America (S&P/TSX1, S&P 5002) to overseas (Emerging Markets and EAFE2,3) during the first quarter of the year. Since the beginning of the year, the MSCI EAFE index has taken the lead with a return of 2.6%, followed by the S&P/TSX at -3.8% and the S&P 500 at -8.5%.

Moreover, within American markets, the technology giants are showing a rare underperformance since the beginning of the year. Indeed, their high valuations make them particularly vulnerable to investor sentiment. This is explained by the fact that stock markets are generally not influenced by absolute results, but rather by results relative to expectations. Therefore, the higher the expectations, the greater the risk of disappointment.

Oil & Gold

The price of oil (US$/barrel) decreased during the first quarter, in a context of increased production in non-OPEC4 countries and relatively weak demand growth. Indeed, as of April 11, WTI5 has declined by 14.2% since the beginning of the year.

Meanwhile, the price of gold2 appreciated considerably at the start of this year. Investors are trying to find refuge in the current geopolitical environment. Gold closed at $3,237/oz on April 11, its historic high. This represents a year-to-date return of 23.3%.

Currencies

Despite the resilience of the American economy and the tariff prospects from the Trump administration, the strength of the US dollar has cooled against the loonie. Indeed, the US dollar has declined by 3.5% against the Canadian dollar since the beginning of the year.

1. The S&P/TSX Index is the primary Canadian stock index measuring the performance of the Toronto Stock Exchange.

2. S&P500, MSCI EAFE and gold returns are expressed in US currency.

3. The MSCI EAFE Index is an equity index designed to measure the performance of equity markets in developed economies other than the United States and Canada.

4. OPEC: Organization of Petroleum Exporting Countries

5. West Texas Intermediate (WTI) Crude oil is the North American standard for setting oil prices. The returns are expressed in US currency.

Investment Outlook

The economy is going through a turbulent period and, although the baseline scenario of our Chief Investment Office still foresees slight economic growth, the probability of a recession has increased.

For markets, volatility is therefore expected to persist over the coming months, allowing time to see where the tariff situation will stabilize, and how the gap between "soft" data (such as consumer sentiment surveys) and "hard" data (such as unemployment insurance claims) will resolve.

Under these circumstances, we believe that this is not the time to opt for a highly concentrated strategy, but rather to favour diversification instead of trying to position oneself based on the decisions of a highly unpredictable US president.

Thus, we maintain a neutral allocation between stocks and bonds, considering that these asset classes present complementary risk profiles and similar return prospects over a twelve-month horizon.

In the face of periods of increased volatility, we often feel a sense of urgency and an impulse to act, fearing that we might miss something important. This urgency is particularly intense when markets collapse - we want to regain control as if we could grab the helm of a ship in distress. However, this impression of being able to influence the situation is merely an illusion of control. In reality, we cannot prevent the market from fluctuating, and it is better to rely on thoughtful investment decisions, made in advance, rather than acting impulsively under the influence of strong emotions during periods of turbulence.

We remain at your complete disposal to delve deeper into these perspectives and enlighten you on your portfolio strategy. We will be delighted to answer your questions and provide you with any clarification you desire.

Sincerely,

Cathy, Guillaume, Marc-Antoine and Inuk

514-871-3474