Your Financial Review of October 2024

Soft Landing?

The third quarter brought good news for investors, with gains across most asset classes. However, stock market volatility was more pronounced than at the beginning of the year. Despite this, several lagging segments, such as Canadian equities and more defensive sectors, managed to rebound. Bonds, meanwhile, performed well during this period.

A surprise rise in the unemployment rate fuelled much of the volatility over the summer months. However, with inflation now "under control," the American Federal Reserve (Fed) responded to the weakening labour market by cutting its benchmark interest rate for the first time since 2020. This marks a shift towards a more accommodative monetary policy. This decision is in line with actions taken by other central banks, notably the Bank of Canada, which has already cut rates three times in response to a more pronounced weakening in the labour market and inflationary pressures on our side of the border.

The reduction in borrowing costs could boost corporate investments and profits, potentially driving up stock prices. Dividend-paying stocks are particularly attractive in a less restrictive interest rate environment, as they offer both potential capital growth and stable income. As companies gain access to cheaper borrowing, they often increase share buybacks and dividends, which supports stock prices.

Ultimately, landing a plane always comes with some turbulence—which is why we're asked to keep our seat belts fastened!—and historical data indeed calls for caution. However, the Fed's stance, stimulus measures in China, and lower energy prices increase the chances that a recession may ultimately be avoided.

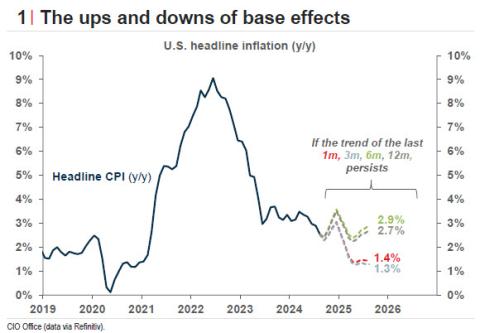

Of course, there is no such thing as zero risk, and less favourable base effects may cause annual inflation to rebound in reports between November and January (see chart 1). However, we still believe that inflation will not be the critical issue in the coming months; the labour market will be.

Market review as of September 30, 2024

Fixed Income

Canadian bonds posted gains for the fifth consecutive month, as the asset class benefited from the rate-cutting cycle initiated by the Bank of Canada at the beginning of the summer.

During the first three quarters of the year, the Canadian bond universe (FTSE Canada Universe Bond Index) delivered a return of 4.27%.

Equities

The economic environment was certainly favourable for equities in September, with all four stock regions posting monthly gains. Investor sentiment was supported by the Fed's "oversized" rate cut.

However, looking at the third quarter as a whole, it's Canadian equities (S&P/TSX1) that topped the leaderboard, while surprisingly, U.S. equities (S&P 5002) ranked last. This trend reversal, observed since the beginning of the summer, is largely due to the underperformance of U.S. tech sectors (communication services, information technology), which reacted to unexpected macroeconomic news, such as policy adjustments in Japan and technological tensions between the U.S. and China.

Nevertheless, U.S. equities are still leading year-to-date with a return of 22.1%. The 10.5% rebound of Canadian equities in the third quarter enabled the Canadian benchmark index to post a year-to-date return of 17.2%, outperforming international equities (MSCI EAFE2,3), which delivered a return of 13.5% over the same period.

Oil & Gold

Gold maintained its excellent momentum and ended the quarter with a growth of 27.5% year-to-date. The price of a barrel of oil (WTI1,4) recorded a decline of 17% in Q3, bringing it into negative territory for 2024 as a whole (-4.4%).

Currencies

Among currencies, the Canadian dollar remained relatively unchanged against the U.S. dollar in the third quarter and is now up 2.1% compared to its level on December 31, 2023.

1. The S&P/TSX Index is the primary Canadian stock index measuring the performance of the Toronto Stock Exchange.

2. S&P500, MSCI EAFE, gold and WTI returns are expressed in US currency.

3. The MSCI EAFE Index is an equity index designed to measure the performance of equity markets in developed economies other than the United States and Canada.

4. West Texas Intermediate (WTI) Crude oil is the North American standard for pricing oil.

Investment Outlook

In the coming months, although lower interest rates fuel hopes of a soft landing for the economy, the outlook remains uncertain. Weakness in the U.S. construction and manufacturing sectors, along with the possibility of another rise in unemployment, could weigh on consumer spending, a key driver of economic growth.

Given this shifting economic landscape, investors should brace for a turbulent period. Equities could experience sustained volatility through 2025, while central banks will act as captains, adjusting course to maintain stability.

In this context, a balanced allocation between equities and bonds remains the wise path. Lastly, we continue to overweight U.S. equities, reflecting our confidence in the resilience of the U.S. market, but we remain vigilant for any developments that may require a change in direction.

For any questions or to discuss your portfolio, please feel free to reach out to us. We are here to support you in this turbulent economic environment.

Sincerely,

Cathy, Guillaume, Marc-Antoine and Inuk

514-871-3474