Your market overview – September Edition

Your market overview – September Edition

Your market overview – September Edition

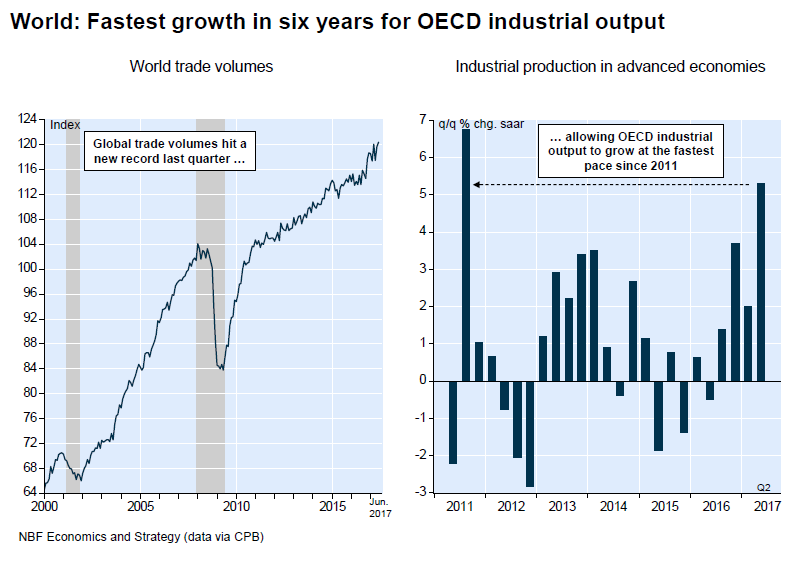

After a dismal 2016, advanced economies are now bouncing back nicely. Latest CPB data shows OECD industrial output surging 5.3% annualized in Q2, the biggest quarterly increase since 2011. That was made possible by a further ramp up in global trade volumes which reached a new record last quarter.

Stronger industrial performance translated into hotter GDP growth in major advanced economies. In the U.S. for example, economic growth accelerated in the second quarter as strength for factories was complemented by continued resilience in the services sector.

Stronger industrial performance translated into hotter GDP growth in major advanced economies. In the U.S. for example, economic growth accelerated in the second quarter as strength for factories was complemented by continued resilience in the services sector.

The U.S. economy continued to expand in the third quarter. July data on employment creation and retail spending were strong, confirming the main driver of growth, i.e. consumers, remain in good shape. Industrial production is also ramping up as businesses replenish inventories and increase investment spending. While hurricane Harvey may subtract a few ticks from Q3 growth, a subsequent rebound led by reconstruction efforts is in the cards. We remain comfortable with our view that U.S. GDP growth will accelerate to more than 2% both this year and next. That should encourage the Fed to further reduce monetary accommodation despite the absence of inflation pressures.

Canada

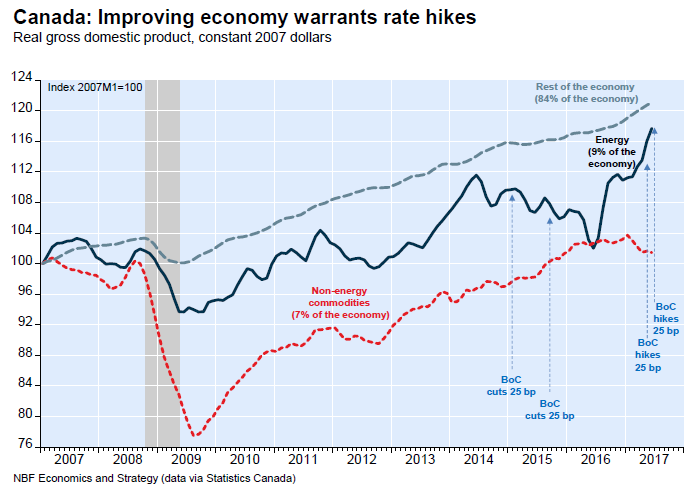

The Bank of Canada raised the overnight rate by 25 basis points to 1.00% at today’s meeting. The central bank supported its decision by pointing to solid growth in consumption, business investment and exports and said growth “is becoming more broadlybased and self-sustaining”. The central bank, however, thought there is still some excess capacity in Canada’s labour market, highlighting subdued wages and prices to prove its point. The Bank of Canada also acknowledged downside risks such as geopolitics and uncertainties with regards to trade and fiscal policy.

A stronger-than-expected first half of the year prompts us to upgrade our Canadian GDP growth forecast for 2017 to 3.0%. Solid growth is being complemented by a healthy labour market, the latter creating jobs in numbers not seen in 7 years. That, coupled with the housing wealth effect ─ consumer credit growth is surging thanks in part to home equity lines of credit ─ is boosting consumption. We have also raised our 2018 GDP growth forecast to reflect provincial fiscal stimulus in Ontario, Quebec and British Columbia. The improving outlook and growing financial stability risks associated with housing and household debt arguably take precedence over the problem of low inflation, and hence warrant tighter monetary policy from the Bank of Canada.

United States

U.S. economic data released in August point to continuing moderate economic growth and strengthening of the labour market in the second half of 2017. The unemployment rate fell to 4.3% in July, one tick below the previous cyclical low reached between October 2006 and May 2007.

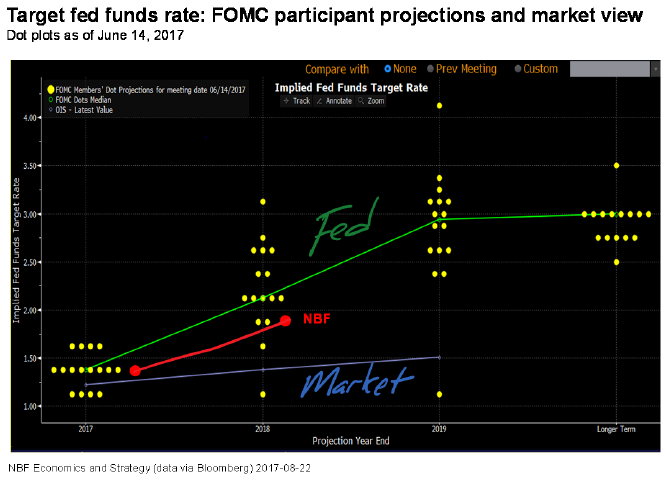

The Fed is not and cannot be a strict inflation targeter. Under current conditions it needs to be cautious about the effect of its policy stance on the stability of the financial system. In the minutes of the July FOMC meeting, the staff assessment of vulnerabilities associated with asset valuation pressures has edged up from notable to elevated. In our view, the Fed must carefully move away from its repression of bond-market term premiums and of financial volatility in general. In its current policy stance, both factors are boosting asset prices and system vulnerabilities. A first step would be to start phasing out its reinvestment of principal repayments from holdings of agency debt and mortgage-backed securities and its rolling over of maturing Treasury securities at auction. The market currently expects Congress to lift the federal debt ceiling before the September 29 deadline, a view that we share. But that is not the only legislative deadline. The 2018 federal fiscal year starts October 1. In our view, the percentage odds of a government shutdown, before hurricane Harvey, appeared to be running in the low 30s. A continuing resolution to fund the government will probably be adopted, but the FOMC may want to wait for its adoption before hiking its target rate again.

Currencies

With economic numbers stronger than expected and the raise of their overnight rate, Canada is now in a position where their currency is set to improve. After having flirted around 1.38 in May, we are now at a level of 1.21 and our team is expecting a range of USDCAD of approximately 1.20-1.30 for months to come. The currency of the European Union was on quite a streak recently, which was a surprise for many experts. This quick hike is happening while the American dollar is losing value compared to other currencies. We can also notice that many investors are afraid that Mr. Trump won’t be able to take forward the tax levels promised, which would lower the expected rate of return of investments in the US.

Asset Allocation

Our asset allocation is unchanged this month. We continue to prefer stocks over bonds. We acknowledge that a failure of the U.S. government to meet the multiple important deadlines on its legislative agenda could be bad for financial markets, especially in the aftermath of Hurricane Harvey. The risk of a stock market correction notwithstanding, we think the economy is on a strong enough footing for companies to deliver on earnings expectations. Geographically, we still prefer Canada over the U.S. given the valuation gap and our view that the CAD will appreciate.

Disclaimer: The opinions expressed herein do not necessarily reflect those of National Bank Financial. The particulars contained herein were obtained from sources we believe to be reliable, but are not guaranteed by us and may be incomplete. The opinions expressed are based upon our analysis and interpretation of these particulars and are not to be construed as a solicitation or offer to buy or sell the securities mentioned herein. National Bank Financial is an indirect wholly-owned subsidiary of National Bank of Canada. The National Bank of Canada is a public company listed on the Toronto Stock Exchange (NA: TSX).