Your market overview - June edition

Market overview

Economy

- The observed uptick in global economic activity is consistent with our view that world GDP growth will pick up to 3.3% this year. Both advanced and emerging economies are seeing stronger growth, although that’s in part due to fiscal and monetary policy stimulus. With tighter policy in the cards for next year, it’s unclear if momentum can extend to 2018, more so considering risks such as trade protectionism, elevated debt levels and the impacts of Brexit.

- The U.S. economy is bouncing back nicely after a rough start to the year. Encouraged by solid employment and the apparent resurgence of industrial output and consumer spending, the Fed will likely raise interest rates again in June. That’s not to say all is rosy. We’re leaving unchanged our forecasts for U.S. growth for now, but acknowledge the possibility that a scandal-hit Trump administration may be unable to deliver the fiscal stimulus it promised.

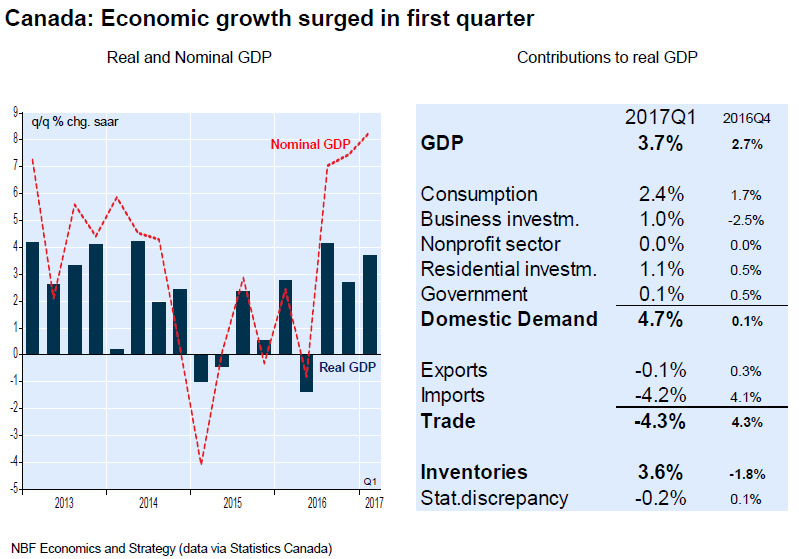

- The better than expected handoff from last year (after upward revisions to Q4) and from Q1 (March’s unexpected output surge) prompted us to raise by two ticks our 2017 growth forecast for Canada to 2.4%. We have also raised our call for next year’s growth to 2%, expecting better business investment and government expenditures, the latter boosted by federal infrastructure money and fiscal stimulus from provincial governments ahead of elections in Quebec and Ontario.

Canada

- The Canadian stock market continues to lag. Declining oil prices, the NAFTA renegotiations, the setbacks of Home Capital Group and Moody's credit rating on Canadian banks all contributed to plunge the S&P/TSX. While we estimate that much bad news is expected at current levels, we advise not to rush on Canadian stocks at this time.

- The 5% drop in oil prices after OPEC members announced an extension of their deal on a nine-month cut last week may sound strange, but we must remember that crude oil follows the same anticipation game than other financial assets. Extension of the term was widely anticipated, but some hoped for more cuts or a restriction on the activities of Libya or Nigeria. Saudi Arabia said that the extension should rebalance the market by itself by the end of the year, which essentially implies that they did not see the need for additional measures.

United States

- The S&P 500 rose to a new all-time high in May, propelled by IT, Utilities, Consumer Staples and Industrials. At this juncture, the outlook for economic growth and profits remains encouraging.

- The U.S. leading economic indicator has been trending up in recent months, suggesting a 2%-plus growth rate in the second half of 2017. Consumption will be buoyed by the addition of more than 1.7 million full-time jobs in the first four months of the year, the best employment growth in more than 20 years.

- The bad news concerning Mr. Trump's pressures with the FBI investigation pushed the S&P 500 down, but the shortfall was quickly closed in six days, allowing the index to generate 1.4% for the month.

- The ‘’Trump Trade’’ continues to slowly she, and small-cap stocks have again underperfomed their larger counterparts.

Forex

Forex

- For its part, the Canadian dollar has moved back into the 1.30-1.35C$/US$ range of November of last year, following stronger economic data, a less dovish stance on the part of the Bank of Canada, USD weakness, and a pick-up in oil prices. Things may continue to evolve positively for the loonie as markets reassess the potential timing of the first rate hike in Canada. But, the immediate trend remains negative for the currency and until we get a clearer view on oil prices developments, our bet is the currency will stay range-bound.

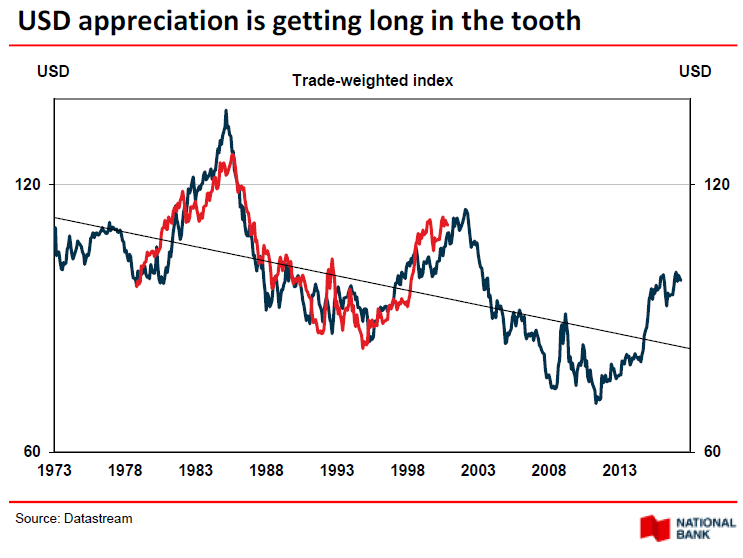

- The way we see things, with monetary tightening well embedded in market expectations, one of two things needs to happen for the currency to resume its uptrend: either the Fed will be more aggressive, or the ECB will postpone the tapering of its monetary purchases to later in 2018. A pre-condition for the former would be for the Fed to start hiking interest rates right at the June 14 meeting. As things look a little bit overdone for the USD, this would likely be conducive to a short-term rebound.

- Historically, however, when the Fed starts a new cycle of monetary tightening, U.S. dollar strength is pretty much in its final innings. Therefore, we wouldn’t be surprise to see the Euro trough around current levels, and gain momentum later on.

Asset allocation

- What really matters is the economic cycle. Based on the expansion phase (that is, years of economic growth following the recovery period), the current cycle seems still short in the tooth. As such, equities should continue to outperform bonds in the medium to long-term horizon.

- In the shorter term however, things are not so clear. Surely, political risks have abated lately. Yet, we can’t help but feel a sense of unease. With North Korea launching missiles, and China being back on the radar, our level of conviction is low.

- Our preference lies in Europe. Certainly, on a stand-alone basis, European markets are also expensive. But, they offer the best relative value versus U.S. markets as they stand at their lowest point since 1970 both on a local FX basis and on USD-adjusted terms.

We remain optimistic for the next few months, but we maintain a high level of security in the portfolios. We are trying to mitigate the risks most likely to occur such as an interest rate hike, a stagnant price for the oil, an underperformance in the North American market and a downturn due to lower than expected earnings.

Disclaimer: The opinions expressed herein do not necessarily reflect those of National Bank Financial. The particulars contained herein were obtained from sources we believe to be reliable, but are not guaranteed by us and may be incomplete. The opinions expressed are based upon our analysis and interpretation of these particulars and are not to be construed as a solicitation or offer to buy or sell the securities mentioned herein. National Bank Financial is an indirect wholly-owned subsidiary of National Bank of Canada. The National Bank of Canada is a public company listed on the Toronto Stock Exchange (NA: TSX).