Your Financial Review of October 2023

Careful Considerations

Careful Considerations

The story of the Summer of 2023 is one of a U.S. economy exceeding expectations. Annual US GDP growth remained above potential and is on track to remain there in the 3rd quarter, leading stock markets to expect a better future for profits, and bond markets to push back the prospect of interest rate cuts.

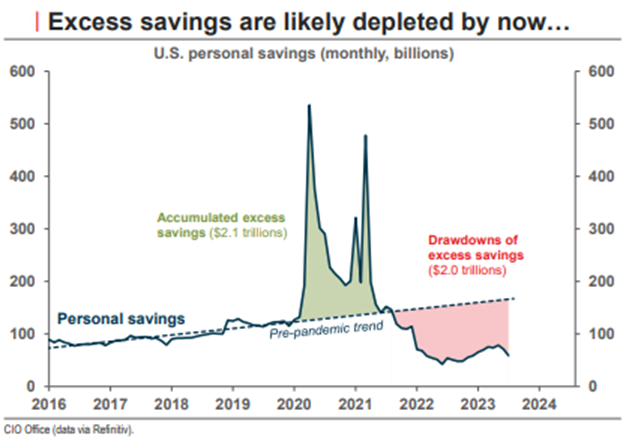

Clearly, the support offered by the prolonged period of ultra-accommodating monetary and fiscal policies persists, with the job market still strong and consumption sustained. In both cases, however, we seem to be nearing a turning point, with the excess savings accumulated in the wake of the pandemic set to become depleted.

During an economic slowdown, we can usually count on fiscal and monetary policy to limit its duration and initiate a recovery. At present, however, the risk is that, having done "too much" in 2020-2021, policymakers seem likely to react belatedly when the next time comes.

In Canada, the story is slightly different. The Canadian economy is showing signs of slowing, with stagnant GDP growth and a weakening labor market. Under normal circumstances, a quarter of stagnation1 in GDP would not necessarily be cause for concern, but the current demographic explosion changes the picture, suggesting that the Bank of Canada's combative rhetoric may not match current economic conditions.

1.Stagnation refers to little economic activity, growth or development. This implies that the economy is not improving and remains at a standstill.

Market review as of September 30, 2023

Fixed Income

- September was a difficult month for the Canadian fixed-income universe, with its 2.6% drop representing the worst monthly decline since April of 2022. This performance was not specific to Canada, however, as bonds in the vast majority of developed countries posted significant monthly losses as yields rose sharply all around the world. This monthly decline brings the year-to-date performance of the Canadian bond market to -1.7%.

- Several factors put upward pressure on bond yields, including disappointing Canadian inflation figures, a Fed that signaled its intention to remain restrictive for even longer, and finally, a major ramp-up in debt issuance by the U.S. Treasury.

Equities

- Following an impressive first half of the year, U.S. stocks (S&P 5002) pulled back in the third quarter to end the month of September with a year-to-date total return of 13.1%.

- Against a backdrop of tightening financial conditions via rapidly climbing interest rates and energy prices, plus significant U.S. dollar appreciation, international equities (MSCI EAFE3) retreated during the quarter, now posting a year-to-date return of 7.6%. Canadian equities (S&P/TSX4) posted a total return of 3.4% over the same period.

- Despite these recent pullbacks, it is important to note that the MSCI EAFE, S&P 500 and S&P/TSX indices yielded significant total returns of around 27%, 22% and 11% respectively since their October 2022 lows.

Oil & Gold

- In the face of persistent supply and inventory pressures, WTI5 oil prices climbed for a fourth consecutive month to their highest level since July of 2022. The price of a barrel of oil was trading at $90.79 (USD) to end the month of September, representing a 13.1% year to date growth.

- The price of an ounce of gold fell in the third quarter, showing a slight appreciation of 2.3% since the start of the year.

Currencies

- The US dollar appreciated against the loonie in the third quarter. However, the USD/CAD pair has remained relatively unchanged since the start of the year, closing September at 1.352 CAD per USD.

2. S&P500 and MSCI EAFE returns are expressed in US currency.

3. The MSCI EAFE Index is an equity index designed to measure the performance of equity markets in developed economies other than the United States and Canada.

4. The S&P/TSX Index is the primary Canadian stock index measuring the performance of the Toronto Stock Exchange.

5. West Texas Intermediate (WTI) Crude oil is the North American standard for pricing oil.

Investment Outlook

On a forward-looking basis, the decisive factor for the markets is likely to be the evolution of the monetary policy stance of major central banks. For the time being, while a rapid fall in inflation would be the best scenario for stocks, and would allow for possible rate cuts, this scenario seems unlikely. Indeed, a certain stagnation—or even an increase—in inflation seems more likely for the rest of the year, which could force policymakers to keep the door open to further interest rate hikes or at least to keep key rates at higher levels for an extended period.

At this time, we believe your defensive asset allocation is still appropriate. We are gradually increasing the duration6 of bond portfolios but remain cautious considering the risk that central banks could maintain a more combative stance on monetary policy as risks of recession increase, hence putting upward pressure on longer-term rates.

6.Duration measures the sensitivity of a bond's value to changes in interest rates, taking into account its maturity, yield, coupon and prepayment clause. Generally, the longer the duration, the higher the sensitivity to interest rates.

Geographically, we continue to underweight international equities, for which the strength of the U.S. dollar and the increasingly apparent weakness of the Chinese economy are major headwinds. On the other hand, the Canadian stock market still seems to us a good candidate for outperformance, benefiting from already compressed valuations.

Moving forward, we will keep a close eye on the evolution of key economic indicators in the event that an adjustment to your portfolio proves necessary.

Do not hesitate to contact us if you would like more information about our outlook or the positioning of your portfolio. It will be our pleasure to review everything at your convenience.

Cordially,

Cathy, Guillaume, Marc-Antoine and Inuk

514-871-3474