Your Financial Review January 2021

Your Financial Review January 2021

Your Financial Review January 2021

While few will miss 2020, all will long remember this past year that began amidst bombings between the U.S. and Iran, featured the worst pandemic in over 100 years, that sparked a recession as brief as brutal.

During the year, we have witnessed the spectacular effectiveness of coordination between monetary and fiscal authorities in times of crisis as well as a succession of historic highs and lows, sometimes quite unusual. In addition, our U.S. neighbors have experienced great social tensions and a presidential election that resembles a referendum on America’s core values.

In summary, 2020 was a year like no other!

Here are some highlights:

Canadian Fixed Income

- The Canadian short Bond Universe (FTSE/TMX Index) posted a return of 5.3% in 2020.

- Substantial cuts in interest rates helped generate good gains for the fixed income asset class. Rates across the entire yield curve hit historically low levels in the first six months of the year following unprecedented monetary stimulus measures taken in response to the global pandemic.

Canadian Stock Markets

- The S&P/TSX Total Return Index (including dividends) ended the year up 5.6%.

- The month of November saw 10 of the 11 sectors of the Canadian market rise significantly which marked the return to a positive performance for the index which until then had been in negative territory!

- The diversity of sector returns was significant with information technology leading the way with an 80% return and the energy sector declining 27% during the year.

- Interestingly, preferred stocks rebounded strongly in the last quarter of the year, ending up with a 6.2% gain for the year.

U.S. Stock Markets

- The S & P500 Index, which is the most representative index of the US stock market, rose 18% in US dollars. Of note, the five tech giants are responsible for more than half of the S & P500's annual performance (Facebook, Apple, Amazon, Google, Microsoft).

- Similar to Canada, the tech sector posted the best performance with 44% return while the energy sub-index fell 34%.

- It must be said that the sectoral composition of the US market played a large part in its favour in 2020, while other indices, such as the S & P / TSX in Canada, have still not crossed new highs.

International markets

- The MSCI EAEO index (Europe, Asia, Far East), for its part, rose slightly by 1.5% in local currencies.

- The region has been held back by its sector allocation which is very oriented towards sectors sensitive to the economy. In doing so, the index's performance lagged over the course of the year until the vaccine announcements were released. Indeed, anticipation of a stronger economic recovery caused the index to jump at the end of the year.

Crude oil

- The price of WTI * oil closed the year 2020 down 21%.

- On a historic note, WTI temporarily traded at negative prices in April of this year, as demand for crude fell sharply due to the first wave of comprehensive containment measures.

* WTI: West Texas Intermediate is a type of crude oil used as a standard in the pricing of crude and as a raw material for oil futures contracts with the New York Mercantile Exchange.

Gold

- The yellow metal continued its 2019 momentum through 2020. Gold rose 25% in US $. The many uncertainties we have experienced during the year have pushed gold to its highest level since 2012. We think the price of gold should remain supported by accommodative monetary conditions and a weaker dollar.

Currencies

- Meanwhile, the widespread weakness of the US dollar has translated into a stronger Canadian dollar. Indeed, the loonie appreciated throughout the year from its low in March. In 2020, it appreciated 2% against the US dollar. The path of least resistance for the US dollar is down. As for the loonie, we believe that it will appreciate modestly over the next 12 months.

2021 Outlook

Economy and stock markets

The new economic cycle should continue its track into the New Year, reinforced by the gradual inoculation of the world's population and supported by more accommodating monetary conditions than ever before. Overall, valuations continue to favor equities, especially when compared to the expected low yield of traditional bonds.

Obviously, each year brings its share of surprises that are, by definition, impossible to predict (e.g.: a global pandemic). Despite this, we can make rational assumptions based on the information currently available.

Here are now the three main pillars on which our outlook is based and some explanations of each one.

Cyclical Conditions

The latest economic data is clear. We are at the start of a new economic cycle that began last May. This does not mean that the economic (and therefore stock market) recovery is immune from any potential incident. If the inoculation rate is too slow and some reinforced and prolonged containment measures are announced, the speed of the economic recovery underway could be altered.

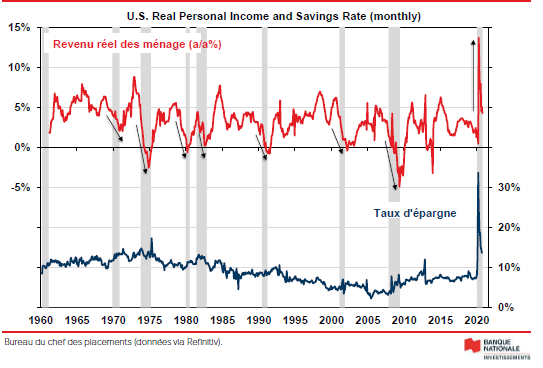

It should be noted, however, that the global economy is already showing considerable resilience despite the persistence of COVID in recent months. This impressive resilience is undoubtedly explained by the unsuspected impact of the fiscal stimulus measures implemented at the start of the crisis and the disposable income of households who saved a large part of it, a situation unprecedented in times of recession (see the graph below).

U.S. households have managed to maintain a reasonable level of consumption in recent months, possibly by tapping into these savings, among other things. Everything suggests that this excess savings should help fuel consumer spending in 2021, to the extent that better control of COVID-19 will ultimately allow a permanent economic reopening and an increase in consumer confidence. Against this backdrop, a strong recovery in corporate profits is expected to be the main driver of stock returns in 2021.

Monetary conditions

The intentions of central banks are clear: to maintain accommodative monetary conditions for as long as necessary to ensure a full economic recovery. Concretely, this means that we should not expect interest rate hikes on either side of the border for the next two years (at least). This is a strong message for the economy and, therefore, for the stock markets.

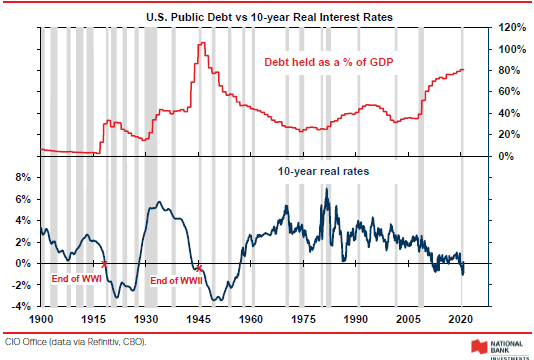

In addition, the U.S. Federal Reserve formalized in the summer of 2020 it’s change of philosophy with regard to inflation, which in itself is a major event of the year 2020. From now on, policy makers will want to see inflation exceed moderately the 2% target for an extended period before even considering a rate hike. Why this change in philosophy? The desired goal is to deflate the burden of debt incurred by governments engaged in the war against COVID-19. Thus, there is little doubt that real rates * will remain negative for several years. This is a similar game plan to that observed after WWI and WWII as illustrated in the following graphic.

* Negative real rate: The real rate is the nominal interest rate corrected for inflation. We speak of a negative real rate when inflation is higher than the nominal rate.

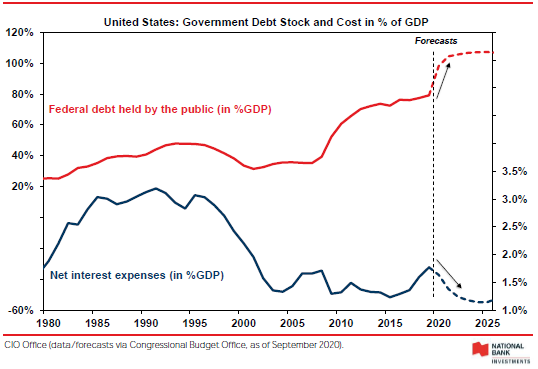

Concretely, despite a good ~ 20% of the federal government's debt level as a percentage of gross domestic product (GDP) in 2020, the cost associated with the total public debt should be lower than it was in 2019 (this is also the case in Canada).

In short, the issue of public debt is perhaps not as heavy as one might think at first glance!

Valuations

Within 12 to 18 months of the end of a recession, earnings growth usually occurs very quickly. Stocks in major markets took part in this improved outlook, but not fully. Maintaining exceptionally low interest rates should help keep valuations above average and make stocks the preferred asset class in 2021.

Even more revealing is a look at the dividend rate of stocks versus the rate of return on government bonds. The spread between the two has not been so favorable to equities since the late 1950s. Could this prompt a number of investors looking for decent returns to switch from the bond market to the stock market on a strategic? This is indeed a theme that we suspect will gain popularity in 2021.

Fixed income

Central banks have pledged to keep short-term interest rates extremely low to support the economy and financial markets, even as the recovery gathers pace. Long-term bond rates could rise a bit, but the upside potential is limited by long-term pressures, such as an aging population, slower population growth, and an increased preference for savings over expenses. All of these have fueled the decline in real interest rates (rates after accounting for inflation) and these trends are unlikely to change anytime soon.

The overall risk / return profile of the asset class is unattractive, especially compared to equities. Against this backdrop, many investors wonder if they should continue to hold bonds in their investment portfolios because of their low interest rates. Although real rates are negative in some cases, the bond market continues to offer relatively better protection against downward movements, as was clearly demonstrated in 2020.

To conclude…

We are optimistic about the future, but we remain cautious about the risks outlined above. In addition, we hope that a change of administration in the United States will not result in significant changes to current policies and that, compared to the previous four years, it will increase stability in terms of geopolitical risk and reduce trade tensions

I hope you enjoyed the New Year edition of our newsletter! Sounda and I reiterate our availability to discuss topics that are important to you. We will have the opportunity to speak together in the near future to follow up on last year's results. In the meantime, we remain available to answer any questions you may have.

Looking forward to talking to you! Please contact us if we can be of any help.

514 871-3474

Disclaimer: The opinions expressed herein do not necessarily reflect those of National Bank Financial. The particulars contained herein were obtained from sources we believe to be reliable, but are not guaranteed by us and may be incomplete. The opinions expressed are based upon our analysis and interpretation of these particulars and are not to be construed as a solicitation or offer to buy or sell the securities mentioned herein. National Bank Financial is an indirect wholly-owned subsidiary of National Bank of Canada. The National Bank of Canada is a public company listed on the Toronto Stock Exchange (NA: TSX). National Bank Financial is a Canadian Investor Protection Fund member (CIPF)