Your Financial Review of April 2026

A Two-Speed Quarter

The first quarter of 2026 saw a notable shift in the economic and financial backdrop. Early in the year, markets extended the positive trends from 2025, supported by still-solid growth and favorable conditions. However, rising geopolitical tensions in the Middle East in March materially changed the picture. This development reshuffled leadership across asset classes, regions, and sectors, and had a particularly pronounced impact on monthly performance, reversing the tone seen earlier in the quarter.

Over the quarter, regional dispersion widened. The Canadian market proved more resilient than most, supported by its status as a net energy exporter and therefore less exposed to higher energy prices. By contrast, European and Asia-Pacific markets, which rely more heavily on oil and gas imports, saw their outlook weaken as tensions persisted. This shift gradually called into question some of the trends established at the start of the quarter.

Commodities were central to the quarter’s dynamics. Energy prices surged on supply disruptions, while precious and industrial metals gave back ground late in the period after a year of strong gains. Even gold, typically viewed as a safe haven, lost some momentum. At the same time, the U.S. dollar strengthened over the quarter, supported both by its defensive role during periods of uncertainty and by higher commodity prices denominated in dollars.

On the macroeconomic front, the quarter closed with elevated uncertainty. Manufacturing indicators remain broadly constructive, reflecting the momentum seen early in the year. By contrast, rising inflation expectations and bond-market moves point to a rapid repricing of energy-related risks. Against this backdrop, central banks have remained cautious, while markets are starting to price in a potentially more restrictive policy path.

In summary, the first quarter of 2026 marks a shift from an environment driven by favorable economic trends to one in which geopolitical and energy factors play a decisive role. This underscores the value of assessing the quarter as a whole, separating early momentum from more recent adjustments, and reinforces the need for disciplined risk management as the second quarter begins.

Market Review as of March 31,2026

Fixed Income

Bond yields faced upward pressure in March, as higher energy prices prompted investors to reassess interest-rate expectations.

In this context, the Canadian bond market (FTSE Canadian Universe Bond Index) finished Q1 2026 slightly higher (+0.23%). Gains built earlier in the year were, however, largely unwound in March.

Canadian corporate bonds (FTSE Canadian Corporate Bond Index) outperformed during March but posted only a modest gain of +0.14% since the start of the year.

Equities

Higher energy prices also weighed on equity markets in March. Most major indices declined over the month, with losses ranging from 4.3% for the S&P/TSX1 to 10.2% for the MSCI EAFE2,3 Index.

Despite March’s pullback, the Canadian equity market (S&P/TSX) ended the first quarter up (+3.9%). This result was driven largely by a strong advance in the energy sector, up roughly 30%. The canadian flagship index led performance year-to-date, followed by international equities (MSCI EAFE: -1.1%) and U.S. equities (S&P 5002 : -4.3%).

Commodities

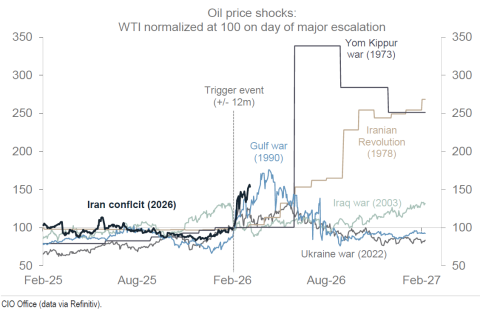

Commodities posted the sharpest moves in the first quarter. The price of WTI4 crude oil rose sharply, up 79.6% year-to-date.

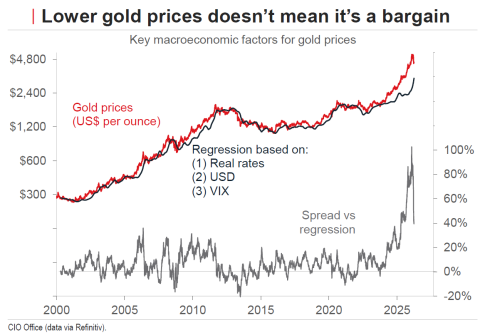

After a strong rise over the past few years, gold2 consolidated in March and ended the quarter with a more modest gain of 6.9% since the start of the year.

Currencies

In March, the U.S. dollar strengthened against most major currencies, supported by its safe-haven role. The U.S. Dollar Index (DXY)2,5 rose 2.4% over the month and 1.7% since the start of the year. This strength weighed on the Canadian dollar, which declined 2% in March and is down 1.4% year-to-date versus the U.S. dollar.

1. The S&P/TSX Index is the main Canadian stock index measuring the performance of the Toronto Stock Exchange.

2. Returns for the S&P 500, MSCI EAFE, the DXY Index, and gold are expressed in U.S. dollars.

3. The MSCI EAFE Index is a stock market index designed to measure the performance of equity markets in developed economies other than the United States and Canada.

4. West Texas Intermediate (WTI) crude oil is the North American benchmark for oil pricing. The return is expressed in U.S. dollars.

5. The U.S. Dollar Index (DXY) is composed of a basket of six currencies weighted against the U.S. dollar. It includes the euro, Japanese yen, British pound, Canadian dollar, Swedish krona, and Swiss franc.

Outlook

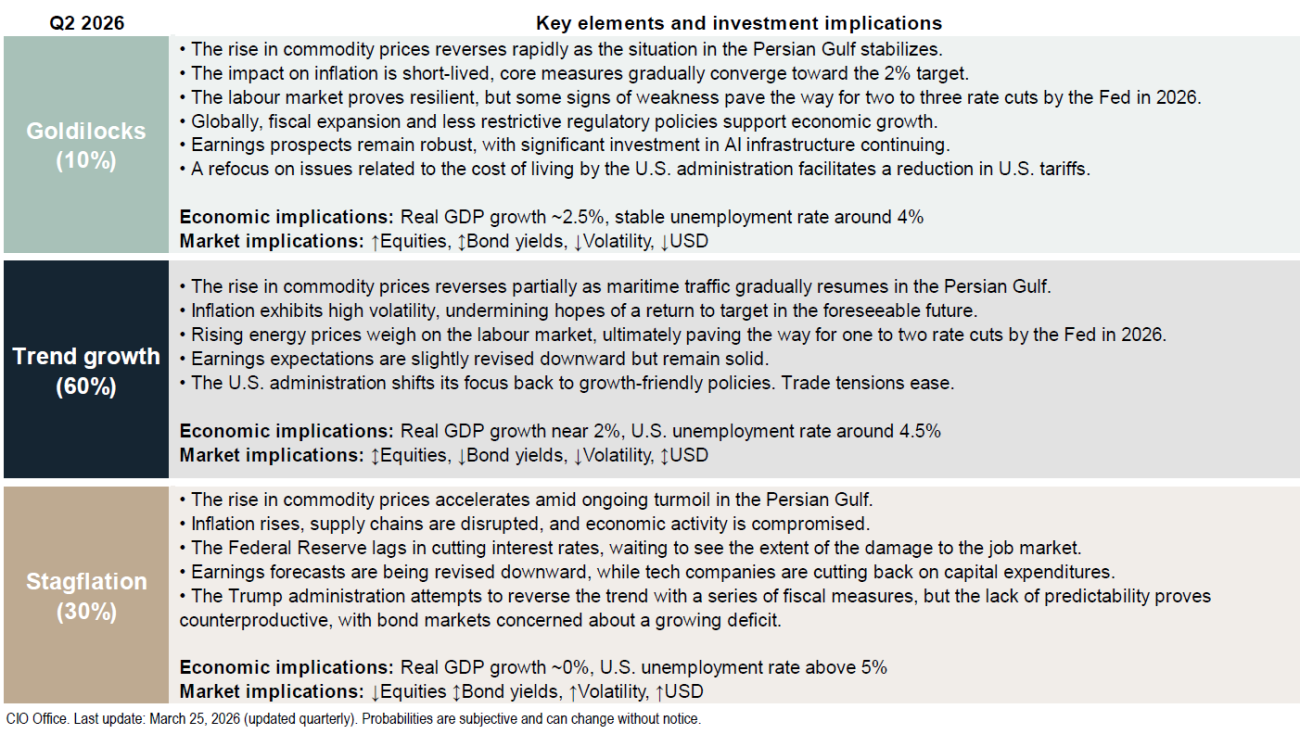

The central scenario of our CIO Office remains continued growth, contingent on a gradual resumption of maritime transport in the Persian Gulf over the near term. In this framework, the dominant risk is not an immediate contraction, but the possibility of a stagflationary shock should the energy and logistics disruption persist, with a heavier drag on global growth. This asymmetry is amplified by the fact that some market expectations appear to assume a swift resolution, increasing sensitivity to any prolongation of the shock.

From an allocation standpoint, the current environment warrants a prudent approach: a neutral equity stance and an increase in fixed income were implemented at the start of the year to better balance portfolios amid uncertainty. For equities, outcomes will depend largely on (i) near-term geopolitical developments and (ii) the trajectory of earnings revisions: de-escalation could support a rebound, whereas a prolonged shock would raise the likelihood of downward revisions. For fixed income, the balance of evidence points to more attractive relative value than before, particularly if risk aversion persists.

In a more uncertain environment, disciplined management, grounded in appropriate diversification and careful risk control, will be essential to balancing opportunity with portfolio resilience.

Thank you for the trust you place in us. We remain at your disposal to discuss these perspectives and to support you as your portfolio evolves, so it stays aligned with your objectives and the market environment.

Sincerely,

Cathy, Guillaume, Marc-Antoine and Inuk

514-871-3474