Your financial review of April 2024

An Economic Fog

Recent months have witnessed some turbulence in global markets, characterized by a series of events that have influenced the economic outlook and investment decisions. As investors digest this new data, it's imperative to take a critical look at the current state of the economy and the trends that could shape the year ahead.

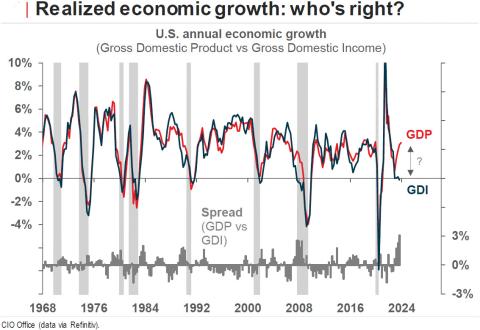

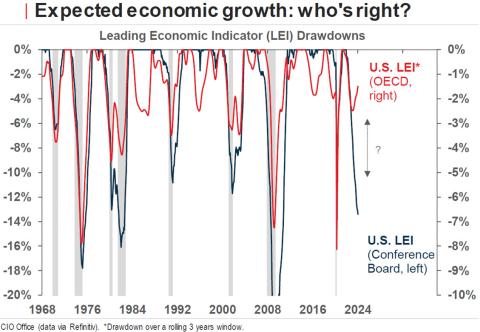

Recent US economic data has been mixed, reflecting increased complexity in interpreting key indicators. Although theoretically identical, readings of economic growth based on gross domestic product (GDP) and gross domestic income (GDI) diverge like never before. Furthermore, leading indicators calculated by the OECD and the Conference Board offer contradictory perspectives on the future. And as if that were not enough, the inflation figures in the United States and Canada add an additional dimension to this analysis. U.S. inflation interrupted its streak of downward surprises, while the opposite occurred in Canada, highlighting persistent challenges to monetary policy and price stability.

In Canada, it is becoming increasingly evident that the rate increases announced since the start of the recent tightening cycle are weighing on the economy. According to the latest Business Outlook Survey published in January by the Bank of Canada, a high number of businesses are reporting a decline in sales, which translates into a weak appetite for hiring. With annual non-shelter inflation down to 1.3%, it is clear that tightening monetary policy has cooled the Canadian economy and labour market over the past six quarters. As the Bank of Canada's latest communications have focused on the resilience of inflation rather than signs of weak growth, there is a risk that it will inflict too much damage on the economy by maintaining an overly restrictive monetary policy.

Market review as of March 31, 2024

Fixed Income

- Although the confirmation of rate cuts intentions by the American Federal Reserve benefited the bond markets in March, the asset class still ended the first quarter in a slight decline after having started the year with high expectations.

- During the first three months of the year, the Canadian bond universe (FTSE Canadian Bond Universe) posted a decline of 1.2%.

Equities

- As in 2023, the first quarter of 2024 proved favourable for the stock market, particularly in the United States. Optimism continued, with the S&P 5001 recording a fifth consecutive month of gain in March as well as its best start to the year since 2019. The flagship American index posted a year-to-date performance of 10.6% as of March 31.

- In terms of leadership, while American and Canadian technology companies continued to do well in Q1-2024, the gains were generally better distributed between sectors. In particular, the energy sector, an important part of the Canadian economy, which has benefited from a rise in oil prices. Despite everything, Canadian equities (S&P/TSX2) have returned 6.6% since the start of the year, outperforming international equities (MSCI EAFE1,3) which have returned 5.9% over the same period.

Oil & Gold

- Following a notable decline in the fourth quarter of 2023, oil prices (WTI1,4) staged a robust rebound in the first quarter of 2024, marking a year-to-date appreciation of 16.8%.

- Gold prices surged in March, buoyed by substantial purchases by certain central banks, heightened geopolitical uncertainties, and impending rate cuts. Notably, the price of an ounce of gold has risen by 7.2%1 since the end of December 2023.

Currencies

- Although currencies remained rather stable in March, the relative strength of the American economy generally benefited the greenback in the first quarter, particularly against the Canadian dollar which ended the period down 2.2% against the USD.

1. S&P500, MSCI EAFE, gold and WTI returns are expressed in US currency.

2. The S&P/TSX Index is the primary Canadian stock index measuring the performance of the Toronto Stock Exchange.

3. The MSCI EAFE Index is an equity index designed to measure the performance of equity markets in developed economies other than the United States and Canada.

4. West Texas Intermediate (WTI) Crude oil is the North American standard for pricing oil.

Investment Outlook

Managing inflation remains a major challenge, with upward pressure on service prices and mixed signals on the stability of supply chains. The manufacturing sector's recovery offers some optimism, although concerns remain about the overall health of the economy.

As we move forward into 2024, it is imperative for investors to remain vigilant and responsive to market developments. As such, it will be necessary to closely monitor the evolution of consumer spending and ultimately, the resilience of the job market, which could be challenged later this year.

By adopting a strategic and diversified approach, we are well equipped to face the challenges and seize the opportunities that come our way. By remaining attentive to market signals and remaining flexible in our investment strategies, we can navigate a complex and uncertain economic environment with confidence. At this time, we judge your defensive asset allocation to still be adequate in the current environment.

From a geographic perspective, we maintain our underweight in international equities due to the strength of the US dollar, restrictive monetary policies and ongoing tensions in the Middle East and Ukraine. On the other hand, the Canadian stock market still seems to be a good candidate for outperformance, benefiting from already compressed valuations.

Feel free to reach out to us if you require further information regarding our outlook or the positioning of your portfolio. We are available to address any inquiries at your convenience and would be delighted to provide clarification.

Cordially,

Cathy, Guillaume, Marc-Antoine and Inuk

514-871-3474