Should I contribute to my RSP or reimburse my mortgage?

Should I contribute to my RSP or reimburse my mortgage?

Should I contribute to my RSP or reimburse my mortgage?

We constantly hear that we should maximize our RSP as soon as financially possible. However, you would also like to get rid of your mortgage and the related monthly payments. What should you do?

The answer relies not only on the financial incentives that confer each savings priority but also depends on your level of comfort with each solution.

Unlike common belief, the principal advantage of an RSP is that your RSP'S investment earnings compound tax-free until they are withdrawn. While many people focus on the upfront tax deduction, tax-sheltered compounding plays an even more important role in building your retirement savings.

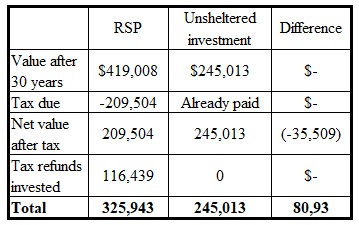

The chart below illustrates these two tax advantages. It compares a $5,000 RSP contribution made at the start of each year to a similar amount invested without tax sheltering. I assumed a marginal tax rate of 50% and a 6% return on both investments.

If your mortgage payments are not tax deductible, then it goes without saying that this form of savings is not as fiscally efficient as the use of an RSP. You now know what is more financially interesting for you.

However, you have to be careful to have an emergency fund and also to make sure your debt payments are not too important compared to your revenues. If all your savings are directed towards your RSP, and your debts make you uncomfortable, we will have to find a compromise between what is more fiscally advantageous and the level of moral comfort and financial security of not having any debts.

Lastly, it will not serve you well to contribute more than necessary to your RSP. A retirement plan done in concert with your investment advisor will allow you to know the amount you should contribute to your RSP each year to get the financial lifestyle you want at retirement.

Please contact me if you would like more information with regards to your specific needs. It will be my pleasure to assist you with your retirement planning.