The potential impact of a Trump presidential victory

The potential impact of a Trump presidential victory

This report examines the potential impact of a Trump presidency in a variety of areas. These include trade relations, the U.S.-China rivalry, tax policy, NATO membership, and green energy initiatives. The report will also look at where a Trump administration would not differ from a Biden administration in terms of policy and what the potential impact of a Trump presidency would be on the American political landscape.

While a Trump administration would mean more protectionism…

A Trump presidency would likely be characterized by increased trade restrictions through support for measures such as a 10% tariff on all imports, which many analysts believe he could implement without congressional approval under the Trade Expansion Act. This law allows a president to enact trade restrictions in response to discriminatory trade practices and for national security reasons.

However, if Trump moved forward to impose a 10% tariff on all imports, he would likely face legal challenges, significant domestic political resistance from members of both parties, and the threat of counter tariffs from other countries.

Reportedly, people in Trump’s inner circle believe he will seek to leverage this tariff threat in order to pressure certain countries to make trade concessions and/or join in trade actions against America’s primary geopolitical opponents. This suggests that the tariff would ultimately be targeted at specific countries rather than applied across the board. Any new tariffs would raise costs on certain products for American consumers.

… it is important to note that support for protectionism is bipartisan.

President Biden's 2021 declaration that "America is back" was welcomed by many countries on the receiving end of Trump's trade sanctions. But to their disappointment, Biden not only kept most of his predecessor's tariffs in place, he added new protectionist measures as well.

Several pieces of legislation that heavily subsidize domestic production of electric vehicles, green energy, and infrastructure are a case in point. While the headline figures show $465 billion being spent on such projects, the actual total is much higher because most of the subsidies are in the form of virtually unlimited tax credits that incentivize domestic production. The Economist has estimated that subsidies could total $100 billion a year over the next decade, roughly double the amount before the pandemic.

As a result, Canada has been compelled to enhance financial support for critical sectors to remain competitive in attracting investments. Notably, Canada has already committed over $40 billion in financial aid for the EV industry alone1.

Finally, it is important to acknowledge that the American public is increasingly in favour of trade restrictions. A recent survey conducted by the Chicago Council on Global Affairs revealed that 66% of Americans believed that there should be restrictions on imports to protect jobs. This was up from 60% in 20182.

China will continue to be the target of increasing trade restrictions

The Biden administration has also followed in its predecessor’s footsteps by imposing ever-tighter trade-related restrictions on China. In 2019, for example, Trump banned the sale of high-end chips to Huawei and a few other key companies. This was escalated by Biden in 2022 when he severely restricted the sale of advanced semiconductors to all Chinese companies.

The Biden administration has also recently announced an investigation into potential data and cybersecurity risks posed by Chinese EVs. China, for its part, has already banned Tesla cars from certain government and military locations, claiming that the car's IT systems could be used to spy on high-level officials.

Trump threatens to further tighten the trade screws on China by reversing America’s decision in 2000 to establish “Permanent Normal Trade Relations” with China. According to Oxford Economics, negating this agreement would increase tariffs on Chinese goods by an average of 61%3. However, given the likely economic shock that the abrupt imposition of such a tariff would cause, it is questionable whether Trump would go through with this plan in full, at least in the short term. A Trump administration might initially target specific sectors in order to further encourage the reshoring of production.

China’s excess production capacity in key areas is another trade challenge on the horizon. A recent article in the New York Times illustrated the magnitude of this problem very well: “China has already built enough solar panel factories to supply the entire world’s needs. It has built enough auto factories to make every car sold in China, Europe and the United States.”4 China will no doubt seek to export its excess capacity, which will trigger a new wave of tariffs from the United States, regardless of who sits in the Oval Office, and from many other countries as well.

Finally, regardless of who is in power, tensions between China and the United States will continue to be driven by a combination of factors, including a great power rivalry, radically different economic/governance models and, most importantly, lack of trust.

Tax and fiscal policy under a Trump administration

In 2017, Republicans lowered federal taxes for both corporations and individuals. While the corporate rate cut from 35% to 21% is permanent, several tax cuts affecting households and small businesses are set to expire at the end of 2025, unless renewed. One of Trump's goals is to make these tax cuts permanent as well.

If Trump is elected and regains control of both houses of Congress, he would be in a very strong position to achieve this goal. This could be accomplished by resorting to reconciliation, a legislative process that allows spending and taxation bills to be approved by a simple majority (50 +1) in the Senate rather than the usual supermajority (60 votes). The Congressional Budget Office (CBO) estimates that making these tax cuts permanent would mean $4 trillion in less revenue over the course of a decade5.

Democrats opposed the law in 2017 but are now in favour of extending Trump’s tax cuts for households earning less than $400,000 while allowing the others to expire. This situation is similar to the one that occurred in 2012 with President Obama. At the time, some of the tax cuts implemented by President Bush were renewed. The most likely scenario in 2025 if the government is divided after the election is that a compromise will be struck between the Republican and Democratic positions.

Tax extensions would be debated against a backdrop of fears over a ballooning national deficit

Although the United States can manage high debt levels more effectively than many other nations thanks to the dollar's reserve currency status, its deep financial markets, its lower operating/energy costs, and its relatively robust economy, it, too, faces constraints. According to the IMF, the country’s gross debt-to-GDP ratio nearly doubled from 2007 to 2022, going from just 62% to 122% (the highest since the end of WWII). What's more, Fitch Ratings expects the ratio of debt interest to tax revenue to reach 10% by 2025. In the event of a significant economic downturn, the country’s fiscal situation would worsen even more.

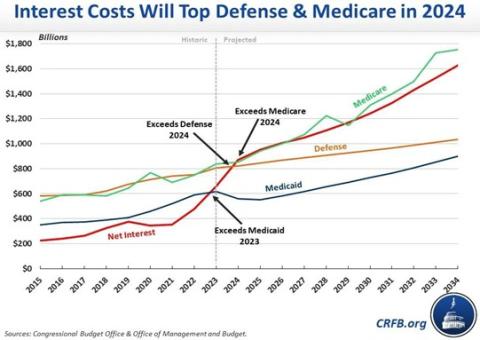

Higher interest rates are already proving a challenge. The CBO has estimated that, in 2024, interest payments ($870 billion) will exceed national defence spending ($822 billion) for the first time on record since 19406.

Both Trump and Biden have firmly pledged not to reduce funding for essential programs like Medicare and Social Security. Trump recently stated: “Under no circumstances should Republicans vote to cut a single penny from Medicare or Social Security.” It would likely take a major crisis for Trump to change his position7. Truth be told, Republicans tend to be fiscally conservative when in the opposition but much less so when they hold the presidency.

How Trump could advance his agenda without congressional approval

One of the first acts of a Trump presidency would be to begin the process of unilaterally reversing certain policies through executive orders. For example:

- Attempt a second time to withdraw the United States from the Paris Climate Accords. Because it takes four years for a country to officially withdraw from this agreement, Biden was able to swiftly reverse course before the time period had elapsed.

- Increase U.S. fossil fuel production by easing the permitting process for drilling on federal lands and encouraging new natural gas pipelines and LNG export facilities.

- Begin the process of undoing certain mandates regarding EV sales and clean energy targets.

Removing, implementing or reversing new executive orders can be a lengthy process. It often takes months or even years to review and respond to potential legal challenges. Typically, these are first heard in federal district courts. The more these cases are heard by Republican-appointed judges, the better the odds that these executive orders will not be overturned.

Another important factor to keep in mind is that during periods of divided government, investors should focus more on who sits atop key regulatory agencies than on bills that often have little chance of becoming law. This is because the heads of regulatory agencies can often implement changes without congressional approval. They can also choose not to strictly enforce existing regulations or laws.

Full repeal of IRA not likely under Republican presidency

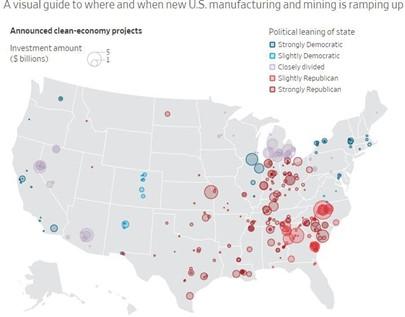

Since the Inflation Reduction Act was passed, over $170 billion in new investments have been announced for green energy projects. Approximately three-quarters of these funds ($113 billion) are projected to be located in congressional districts held by Republicans8. These investments cover various initiatives, including the production of EVs, solar panel components, electrical grid equipment, and mining of critical minerals. Even if the Republicans were to control the presidency and both houses of Congress, it would be politically very difficult for many Republicans to adopt a position in favour of cutting financial support for these projects.

Despite what politicians promise on the campaign trail, history teaches us that even when laws, subsidies, or tax cuts are enacted strictly along party lines, they tend to be remarkably resistant to repeal. Notable examples include the Affordable Care Act (Obamacare) and Trump’s 2017 tax cuts.

However, Republicans are likely to push for stricter requirements to qualify for EV and alternative energy subsidies. One possible change would be to eliminate the exemption that currently allows leased vehicles to bypass local content requirements needed to qualify for tax credits. J.D. Power, a consumer intelligence firm, found that leasing accounted for 26% of all EV transactions in July 2023, up from 7% in December 2022.

Is Trump’s bark bigger than his bite when it comes to NATO?

While a Trump administration would exert significant pressure on NATO members to boost defence spending, the chances that it would actually attempt to withdraw the United States from NATO are very slim for several reasons:

- In 2017, at his first NATO summit, President Trump accused allies of essentially taking advantage of America. The following year, however, his tone changed dramatically: “The people have stepped up today like they’ve never stepped up before… $33 billion more they’re paying. Everybody in the room thanked me. There’s a great collegial spirit in that room that I don’t think they’ve had in many years.”9

- Trump is known for making bold and inflammatory public statements that often lead to less drastic outcomes. For example, his threat to dismantle NAFTA led to a renegotiated deal (USMCA) with major but not transformative changes.

- There is a strong bipartisan consensus regarding the importance of NATO. This is highlighted by Congress recently passing legislation—awaiting President Biden’s signature—that prevents any U.S. president from unilaterally withdrawing from NATO without congressional approval.

But the longer the impasse in the United States over aid to Ukraine continues, the greater the fear in Europe that a divided America lacks the commitment to fully defend its allies.

Improving military readiness a challenge for Europe

Europe has sought to deflect criticism that it is underspending in defence by correctly pointing out that 18 of the 31 NATO members are on track to hit the 2% of GDP spending target in 2024, up from three in 2014. However, achieving the 2% target will not make up for the many years of underinvestment by many countries. For example, West Germany had over 7,000 tanks in the 1980s, versus only 200 today10.

McKinsey has estimated that over the past three decades, European NATO members have collectively spent $1.6 trillion less than would have been the case had they consistently allocated 2% of GDP to defence11.

Europe defence spending vs. social safety net

Europe will also face growing difficulty balancing the need for increased defence spending and financial support for critical industries with the public's demand to maintain and even expand the social safety net. France is a case in point. Soon after announcing a substantial hike in defence spending last year, the government faced extensive protests when it implemented minor cuts to the national pension system. Farmers across Europe protesting environmental regulations and cuts to financial aid is another example. We believe these are just the first of many other similar situations to come.

Canada’s massive defence challenge

When it comes to defence spending, Canada ranks near the bottom among NATO members. Currently, Canada spends 1.3% ($26.93 billion) of GDP on defence. According to calculations by the Parliamentary Budget Officer, Canada would need to boost spending by $14.5 billion to reach the 2% target in fiscal year 2024-2512. Increasing defence spending is one of the most important things Canada could do to get on the right side of a potential Trump administration.

However, one of the biggest challenges to a massive increase in defence spending is public opinion. A recent Global News/Ipsos poll found that military issues are of concern to only 7% of Canadians, while nearly half say the cost of food should be the government's top priority, followed by inflation and interest rates (45%) and access to affordable housing (39%)13.

The Ukraine war

While a Trump administration would put more pressure on Ukraine to negotiate with the Russians, it is important to keep in mind that, regardless of the outcome of the U.S. election, significant territorial expansion remains a challenge for Ukraine. This is due to Russia’s deeply entrenched defences, which include an extensive network of mines, trenches, and traps along the front line. There are also growing signs that the American public's support for continued financial assistance to Ukraine is beginning to soften.

Any settlement would likely result in a "frozen conflict" rather than a formal peace, with Russia retaining control of most of the occupied territories. This in turn could lead to demands from the West for further financial assistance to rebuild Ukraine and its economy, as well as provide increased military aid to protect against future attacks.

Will the USMCA be renewed?

The first six-year review of the trade agreement will take place in 2026. If the three members cannot agree on a renewal, the agreement would expire in 2036. While a Trump presidency would likely raise certain issues, the risk of the USMCA being terminated is very low for two reasons. First, a 2036 expiration date gives the three countries plenty of time to negotiate and reach a new agreement. Second, Trump has repeatedly claimed USMCA as one of his crowning achievements.

Another significant hurdle to terminating the United States-Mexico-Canada Agreement is the high level of economic integration among the three economies. Products frequently cross borders multiple times during the production process before reaching the final stage. For example, while only about 4% of the components in Chinese imports originate from the United States, a substantial 40% of Mexican imports are manufactured with U.S.-sourced parts14.

However, there are growing concerns in the United States that China is trying to avoid U.S. tariffs by rerouting shipments and/or moving some final assembly production through Mexico first. Of particular concern are plans by Chinese EV manufacturers to open factories in Mexico. Cars and parts assembled in Mexico are subject to tariffs of 2.5% and 0 to 6%, respectively, when imported into the United States. By contrast, cars and auto parts imported directly from China are hit with a 25% tariff (which the Biden administration is considering raising). A Trump administration would very likely push to close this loophole in the trade agreement15.

Mexico-U.S. relations will nonetheless be tested

In an effort to curb the flow of drugs and illegal immigration into the United States, it is very possible that a President Trump would designate drug cartels as terrorist entities via executive order. Such a move would grant law enforcement and prosecutors increased authority to freeze cartel assets and more deeply scrutinize company records. This, in turn, could significantly increase wait times for Mexican goods entering the United States.

Back in 2019, President Trump refrained from classifying Mexican drug cartels as terrorist organizations at the personal request of Mexico’s President. However, there is much more support in the Republican Party for this today. To cushion the blow of such a measure, Mexico would likely have to significantly increase cooperation on fighting cartels and illegal immigration.

The American political landscape

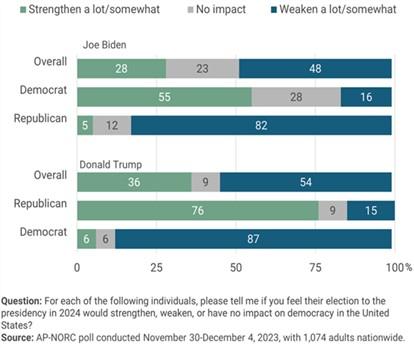

U.S. presidential elections are often closely contested affairs, and the losing side may find it difficult to accept the outcome. This time around, the risk is exacerbated by what some people call the criminalization of political differences, where the partisans of each political party accuse the other side of corruption while ignoring their own transgressions. Moreover, a recent poll showed that over 80% of Democrats and Republicans believe that a win by the other side would weaken democracy. All of this increases the risk of protests by supporters of the losing side, particularly if the election is close. This would in turn add to an already highly polarized political landscape.

There is also the risk of a constitutional and/or political crisis if Trump wins and is later convicted in one of his court cases. For example, the U.S. Supreme Court’s decision to consider Trump’s appeal for Presidential immunity means that the trial based on allegations of attempting to overturn the 2020 election results will probably be delayed until the fall. Consequently, the likelihood of a verdict being reached before the November election is increasingly slim.

Bottomline

If re-elected, President Trump would seek to further many of the policies of his first term. However, his re-entry into the Oval Office would coincide with a period of escalating global geopolitical tensions and growing domestic political discord. As a result, investors should closely examine how this new landscape would affect the market’s reaction to his policies.

-

“In giving billions to electric car makers, Canada is blinded by economic delusion,” The Globe and Mail, February 12, 2024

-

“Donald Trump’s second term would be a protectionist nightmare,” The Economist, October 31, 2023

-

“How scared is China of Donald Trump’s return?” The Economist, February 20, 2024

-

“More Semiconductors, Less Housing: China’s New Economic Plan,” New York Times, November 6, 2023

-

“Trump tax cuts on the line in 2024 election,” The Hill, February 21, 2024

-

“Do We Spend More On Interest Than Defense?’” Committee for a Responsible Federal Budget, February 20, 2024

-

“Trump warns U.S. House Republicans not to touch Social Security, Medicare,” Reuters, January 20, 2023

-

“Biden’s Green Factory Push Is Benefiting Republican States,” Wall Street Journal, February 27, 2024

-

“Nato defence spending to hit record as alliance braces for potential Trump win,” Financial Times, February 14, 2024

-

“Alarm grows over weakened militaries and empty arsenals in Europe,” Wall Street Journal, December 11, 2023

-

“How Prepared Is the German Defense Industry,” Spiegel, February 16, 2024

-

“Our military isn't prepared for a new era where geography doesn't shelter us: Canada Undefended,” National Post, February 15, 2024

-

“Canada must realize that a strong economy comes from a strong military,” The Globe and Mail, December 13, 2024

-

“‘OK, Mexico, Save Me’: After China, This Is Where Globalization May Lead,” New York Times, January 1, 2023

-

“China circumvents US tariffs by shipping more goods via Mexico,” Financial Times, February 21, 2024