1st Quarter 2017 : Our summary of the market

Our summary of the market

Our summary of the market

FINANCIAL MARKETS

With Donald Trump establishing his new headquarters in the oval office and the conflicts in the South China Sea, the year 2017 started on a very eventful beginning. The financial markets reached new highs and maintained a low level of volatility.

This constant progression has been generated by the recovery of the World economy, good investors’ expectations of the fiscal stimulus proposed by Trump, the ascent of the basic materials’ prices and the important job creation in the United States.

The Dow Jones Index recently reached a new high of 20 840 points on the 23rd of February and the S&P/TSX had gone up close to the 16 000 points level a few days before.

Also, several businesses presented their financial results for the period ending in 2016 and these results were, for the most part, well perceived by the market which stimulated the market even more. The financial and basic material sectors had a lot of momentum and played a major role in the ascent of the market.

At the end of this quarter, the Trump administration got its first major setback with the failure to repeal Obamacare. The uncertainties about the electoral promises made by Trump are starting to emerge again.

In Canada, The Toronto Stock Exchange also suffered a slight correction caused by a drop in the oil and basic materials prices. The oil prices went down following the OPEC announcement about the rising oil inventories in developed markets.

Considering the actual economic cycle, the expansion that we just witnessed during January and February will be difficult to sustain. Even if there is still a potential gain to be made, it is fairly limited because of several factors like the expensive price of the stocks and the number of consecutive years of expansion on the financial markets which comes at an historical end.

ECONOMY

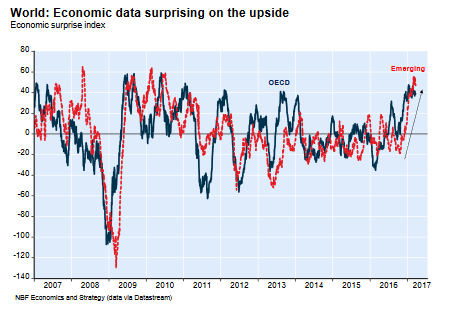

As we explained earlier, the world economic activity seems to have turned the corner during the beginning of 2017. The increase in the U.S labor market and the rebound of the emerging markets provided stimulus to the expansion of the world production.

Canada

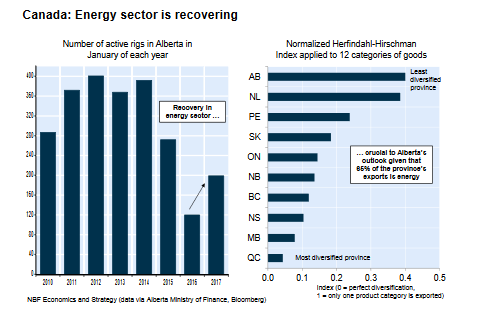

At home, the diversification efforts with other countries than the United States are considerable. The recent economic and commercial agreement with the European Union is a good example of those efforts. The energy sector is slowly recovering and we noticed an increase in the number of active rigs in Alberta. Also, following recent announcements, the exports seem to have grown while imports most likely dropped a little.

For the rest of the year to come, many factors have positive perspectives and will fuel the expansion of the economy. First of all, we believe that the oil prices should stabilize and stay in a range of $45 and $60 USD which would stimulate the energy sector. Furthermore, the new Trump administration seems to be promoting the Canadian oil exports with the signature and approval of the construction of the Keystone XL pipeline project. Next up, with the signature of the new economic agreement with the European Union, the manufactory exports should be growing and increase the GDP. Also, the latest economic statistics showed strong consumption and job creation during the first quarter of 2017.

For the rest of the year to come, many factors have positive perspectives and will fuel the expansion of the economy. First of all, we believe that the oil prices should stabilize and stay in a range of $45 and $60 USD which would stimulate the energy sector. Furthermore, the new Trump administration seems to be promoting the Canadian oil exports with the signature and approval of the construction of the Keystone XL pipeline project. Next up, with the signature of the new economic agreement with the European Union, the manufactory exports should be growing and increase the GDP. Also, the latest economic statistics showed strong consumption and job creation during the first quarter of 2017.

On the other hand, the enterprises’ investments were still very low mostly because of the uncertainties around the commercial and fiscal policies of the American administration.

Very recently, the federal and provincial governments presented their 2017 budgets.

For the federal, the government didn’t want to implement major changes in order to wait and follow the developments on the other side of the border. One thing to notice is that the rumors stipulating that the taxation of the capital gain would increase from 50% to 75% didn’t materialized themselves.

For the provincial, the elimination of the health contribution for low- and middle-income taxpayers and the increase of the basic personal amount for tax credits were the more significant changes for the individuals. For the businesses, the introduction of an additional capital cost allowance of 35% for electronic equipment and software purchases will be implemented.

United States

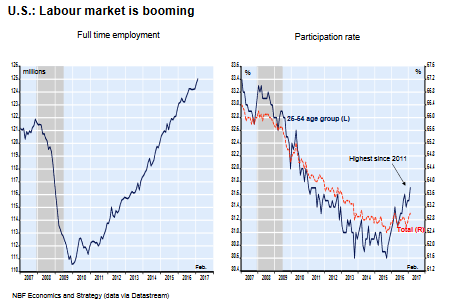

In the United States, the expansion of the economy has mostly been based on job creations. With the recent announcements of the new Trump administration, the businesses have regained a little confidence and hired massively. With the current affordable interest rates and the good news in the labor market, the consumers still extend their spending behavior.

All told, the fiscal stimulus proposed by Donald Trump will most likely contribute to the expansion of the U.S GDP and the inflation will without a doubt start pressuring the economy. These inflationary pressures should constrain the Fed to put in place three increases in the interest rates during 2017. Still, the Fed may be tempered by the likely moderation in the pace of job creation for the next several months. That being said, we estimate that the American GDP growth should be around 2-3% in 2017 which is lower than the promise of 4% made by Trump during the elections.

All told, the fiscal stimulus proposed by Donald Trump will most likely contribute to the expansion of the U.S GDP and the inflation will without a doubt start pressuring the economy. These inflationary pressures should constrain the Fed to put in place three increases in the interest rates during 2017. Still, the Fed may be tempered by the likely moderation in the pace of job creation for the next several months. That being said, we estimate that the American GDP growth should be around 2-3% in 2017 which is lower than the promise of 4% made by Trump during the elections.

Furthermore, the indebtedness now reaching the same level as the crisis of 2008 isn’t as risky as it was before the crisis because of the major decrease in the households’ credit portion of the total debt.

Euro Zone and Emerging Markets

In Europe, despite heavy protectionist pressures, the economy continued to expand during the beginning of 2017. The progression comes from the improvement of the businesses’ confidence towards the world economy and leading to hiring boost.

Even with these encouraging news, the Brexit and protectionism are still major sources of uncertainties and applying pressure on the European Union. Very recently, the United Kingdom officially started its dissolution from the European Union and the negotiations are going to be complex and challenging for both parties.

Important matters to follow in the coming months in Europe are the growing interest for protectionism which could lead to major consequences for the global economy.

In regard to the emerging markets, these economies seem to be recovering after a tough year in 2016. China mostly contributed to the rebound of the expansion of the economy because of an increase in exports. The Latin America economies are improving and showing good perspectives for the rest of the year. We are closely monitoring the US dollar because its appreciation would have a negative impact on these countries knowing that most of them have US dollar denominated debts.

In regard to the emerging markets, these economies seem to be recovering after a tough year in 2016. China mostly contributed to the rebound of the expansion of the economy because of an increase in exports. The Latin America economies are improving and showing good perspectives for the rest of the year. We are closely monitoring the US dollar because its appreciation would have a negative impact on these countries knowing that most of them have US dollar denominated debts.

Asset allocation

A small note on the fixed income products, we believe that they are exposed to significant risks because of the incoming increase in the interest rates in response to the growing inflation. The oil prices are now significantly higher than last year and the labor market is strong enough to fuel the growth of the salaries. These factors are going to be the main reasons for the rise in inflation during the year. The Federal Bank has already increased its official rate in March and more hikes are expected for the next quarters. Knowing that, we strongly suggest to invest in short term bonds and non-traditional fixed income products offering a better protection in a context of interest rate rises. If investing in long term products is required, we would consider inflation hedged investments. Furthermore, we don’t expect a recession in 2017 and believe that risky assets will have a stronger performance than government bonds.

The divergence between the Federal Bank monetary policy and the other central bank should most likely generate an escalation of the US dollar. The US currency would also be stimulated by the protectionist policies implemented by the Trump administration. Therefore, the Canadian dollar will probably be under pressure. This idea is reinforced by the fact that the recent performance of the currency has mostly been influenced by the strength of the US dollar and less by the fluctuations in the oil prices.

Considering this is the 9th year of the market cycle, our strategy is to progressively take profits on equities as the market continues his bullish pattern continuously beating its all-time highs.

Disclaimer: The opinions expressed herein do not necessarily reflect those of National Bank Financial. . The particulars contained herein were obtained from sources we believe to be reliable, but are not guaranteed by us and may be incomplete. The opinions expressed are based upon our analysis and interpretation of these particulars and are not to be construed as a solicitation or offer to buy or sell the securities mentioned herein. National Bank Financial is an indirect wholly-owned subsidiary of National Bank of Canada. The National Bank of Canada is a public company listed on the Toronto Stock Exchange (NA: TSX).